Loading…

Loading…

Every Indian company has to depreciate the same asset two different ways. Here's how ERPNext keeps both books straight — on one set of transactions, without a parallel spreadsheet.

Every company in India carries the same fixed asset on two different depreciation schedules at once — one for the financial statements it files under the Companies Act, and a completely different one for the return it files under the Income Tax Act. The methods differ, the rates differ, the asset groupings differ, and the numbers almost never match. Most finance teams reconcile this the hard way: the ERP runs one schedule and a spreadsheet quietly runs the other. This paper explains how ERPNext solves it natively with Finance Books — named parallel ledgers that let you post and depreciate the very same assets and transactions under several sets of rules at once. We ground it in the actual ERPNext doctypes: the Finance Book master, and the Asset Finance Book that holds a separate depreciation method, rate and useful life per book on a single asset. The goal is to show CFOs and controllers what the software genuinely does, what still needs judgement, and where an experienced partner earns their keep.

The complete paper — every section, in a clean branded PDF you can share with your team. Free, no email required.

Because two different laws apply. Depreciation in the financial statements you file with the Registrar of Companies follows the Companies Act, which is framed around each asset's useful life. Depreciation you claim on your income-tax return follows the Income Tax Act, which uses prescribed rates on blocks of assets on a written-down-value basis. The two legitimately differ on method, rate and grouping, and that gap feeds deferred tax — so the same asset carries two schedules at once.

A Finance Book is a named ledger — essentially a tag — that lets a single set of accounts and assets be recorded and depreciated under more than one set of rules at the same time. It is not a separate company, chart of accounts or database. You create one Finance Book per regime you must report under (for example, one for your statutory accounts and one for income tax), and transactions such as Journal Entries carry a Finance Book field so entries can be directed to a specific book or, if left untagged, applied to all books.

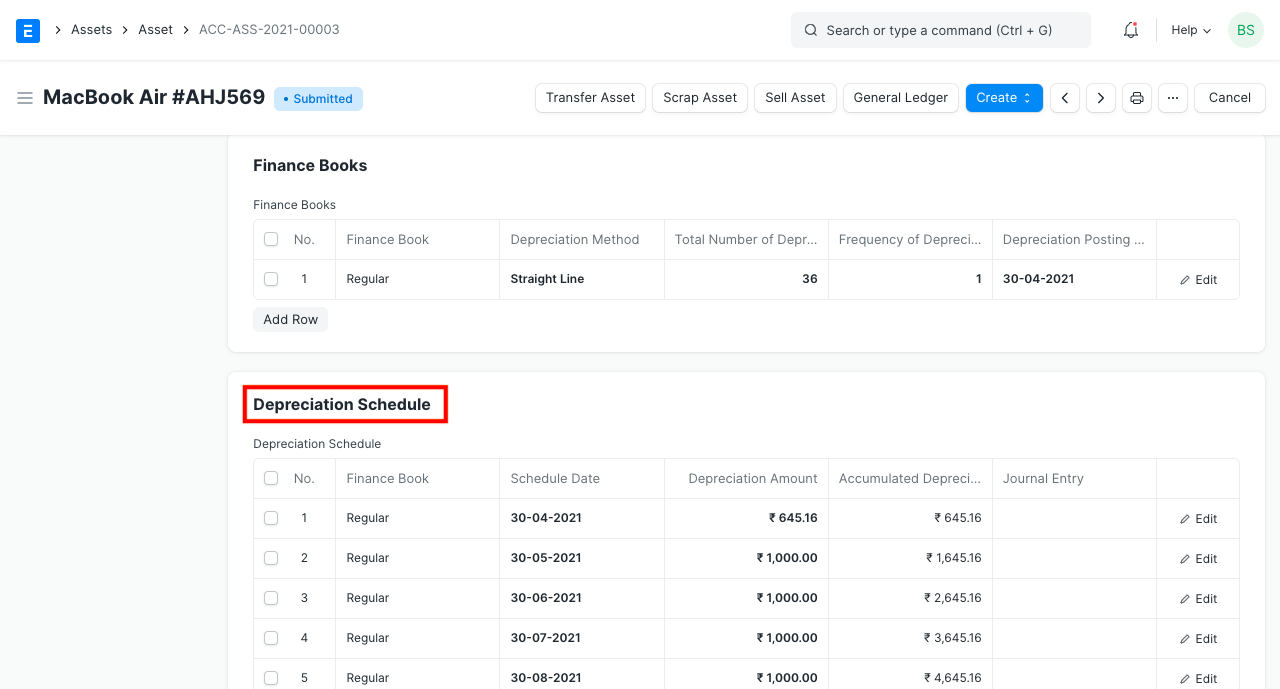

Yes. On a single asset, ERPNext's Asset Finance Book child table holds one row per Finance Book, and each row is an independent depreciation configuration — its own method (Straight Line, Written Down Value, Double Declining Balance or Manual), its own useful life (total number of depreciations and frequency in months), its own rate of depreciation and salvage value. ERPNext then generates a separate depreciation schedule per book, so one asset record satisfies both the Companies Act and the Income Tax Act without duplicate masters.

ERPNext gives you the parallel accounting and depreciation ledgers cleanly — both books are computed and posted from one set of transactions, and you can report each book separately. The deferred-tax reasoning that sits on the gap between the two books, and India's specific block-of-assets treatment on the tax side, remain professional judgements your finance team and auditors own. The value is that those judgements are made from figures you can trust, rather than by reconciling an ERP against a shadow spreadsheet.

Get a clear plan, an honest timeline, and a fixed scope. Talk to a real expert today — whether or not you work with us.

Kochi (Kadavanthra & Infopark) · Thiruvananthapuram · across India & overseas · In business since 2011